Key Takeaways

- Start saving early to maximize the benefits of compound interest.

- Adapt investment and savings strategies for each life and career stage.

- Monitor legislative changes affecting retirement accounts and contributions.

- Schedule regular reviews and updates to your retirement strategy to stay on track with your goals.

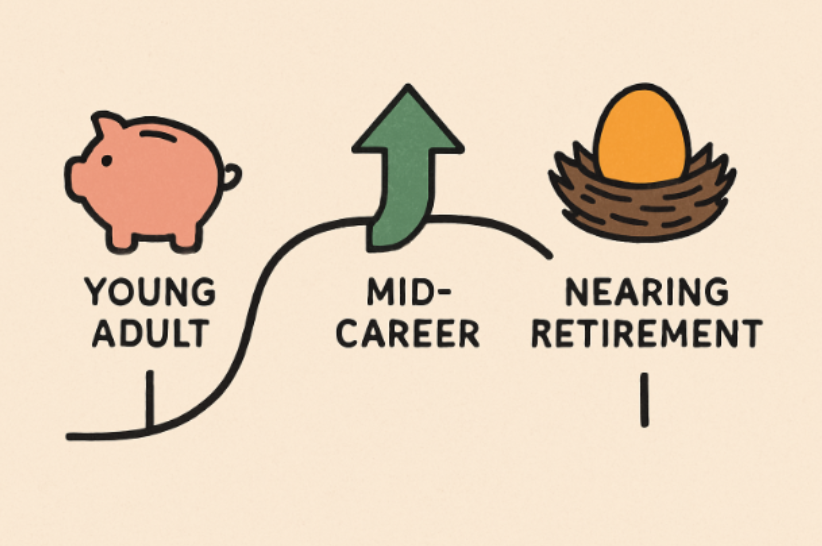

Retirement planning doesn’t have a one-size-fits-all formula. Each phase of life presents distinct opportunities and challenges, making it essential to employ strategies tailored to both your current circumstances and your long-term objectives. From leveraging the power of compound interest early in your career to optimizing catch-up contributions before retirement, a step-by-step approach helps build a future where you can retire confidently. When exploring guidance and options, consider the benefits of planning for retirement with ADP, which offers solutions to help you navigate the complexities of retirement savings at every stage of life.

Taking control of your financial destiny starts with making smart moves and informed decisions as early as possible. Even if retirement feels far away, the actions you take today will shape your financial freedom tomorrow. Understanding how your needs change throughout your working life—and adapting your plan accordingly—is key to long-term security and peace of mind.

Starting Early: The Power of Compound Interest

If you’re in your 20s or 30s, time is on your side. Compound interest means you can earn interest not just on your contributions, but on the interest those contributions accrue. The sooner you begin saving—even in small amounts—the more you stand to gain due to this exponential growth. For example, consistently saving $200 per month from age 25 can result in a substantial retirement fund by age 65, simply because those early investments have decades to grow.

Automating your savings and prioritizing retirement contributions now can help you build disciplined habits and benefit from market growth across economic cycles. Young professionals who start with employer-sponsored plans, like 401(k)s, often find themselves better positioned to weather short-term market fluctuations and capture long-term gains. For more detailed guidance on financial fundamentals in your early working years, consult trusted sources such as Investopedia’s Guide to Retirement Planning.

Mid-Career Adjustments: Maximizing Contributions

By your 40s and 50s, your earning power often increases, providing room to ramp up your retirement savings. It’s a good idea to revisit your contribution rates and consider the benefit of maximizing your annual allowances for retirement accounts. In 2024, individuals under the age of 50 can contribute up to $7,000 annually to a Roth IRA, and those aged 50 or older are eligible for an additional $1,000 in catch-up contributions.

If you’re participating in a 401(k), take full advantage of any employer match—this is essentially “free money” that accelerates your savings. Also, diversifying your investments is increasingly important at this stage. Balancing higher-growth stocks with more stable bonds can help manage risk as your retirement horizon gradually shortens. Learn more about these strategies at Forbes: Mid-Career Retirement Planning Tips.

Approaching Retirement: Catch-Up Contributions

Once you reach age 50, the IRS lets you make “catch-up” contributions, enabling you to save more in the years just before retirement. Legislation such as the SECURE 2.0 Act has expanded these contributions, allowing individuals aged 60 to 63 to make even larger “super” catch-up contributions to specific plans. Seizing this opportunity is vital if you feel behind or want to give your nest egg a last-minute boost while taking advantage of tax advantages.

Understanding Key Milestone Ages

Age-based milestones play a massive role in retirement planning, especially as you near retirement. Here’s a quick guide to pivotal ages:

- Age 50: Eligible to make catch-up contributions.

- Age 55: In some circumstances, penalty-free withdrawals from retirement plans can begin if you leave your job.

- Age 59½: Withdrawals from most retirement accounts are no longer subject to early withdrawal penalties.

- Age 62: First possible age to claim Social Security benefits, but doing so results in reduced benefits.

- Age 65: Eligible for Medicare coverage starts.

- Age 73: Required Minimum Distributions (RMDs) must begin for many retirement accounts under current law.

Understanding these landmarks helps you plan distributions, avoid penalty expenses, and make the most of your retirement savings.

Staying Informed: Legislative Changes

Retirement laws and regulations are continually evolving in response to shifts in the economy, political priorities, and the needs of an aging population. These changes can significantly influence how individuals save, invest, and withdraw their retirement funds. Recent legislation, including SECURE 2.0, illustrates this evolution by adjusting the age at which Required Minimum Distributions begin and expanding opportunities for catch-up and employer-sponsored contributions. Such updates can affect both short-term planning decisions and long-term financial outcomes, making it essential to stay informed. Relying on authoritative resources—such as government websites, financial regulatory agencies, and trusted financial advisors—helps ensure your retirement strategy remains compliant, efficient, and aligned with current rules.

Regular Review and Adjustment

Your financial circumstances can change significantly over the course of five or ten years, making it essential to reassess your long-term plans on a regular basis. Major life events—such as job transitions, marriage, growing a family, or even shifts in the broader economy—can all influence how much you save, how you invest, and what you need for a secure retirement. These transitions may require adjustments to contribution levels, risk tolerance, or investment strategy. Meeting with a financial advisor consistently provides clarity and direction, helping you stay aligned with your evolving goals. Advisors can also help you identify new opportunities, anticipate potential challenges, and adjust your portfolio to mitigate emerging risks. By revisiting your plan regularly, you maintain control and stay prepared for whatever the future brings.

Conclusion

The path to long-term retirement security is a gradual process that evolves throughout your working life. Laying the foundation early with consistent saving allows your investments more time to grow, giving you a significant advantage later on. As you enter your mid-career years, consider increasing your contributions, taking advantage of employer matches, and exploring additional investment options to accelerate your financial progress. Approaching retirement, it becomes even more critical to use catch-up contribution provisions and stay updated on policy or legislative changes that may affect your savings strategies. Remaining informed helps you adjust your plans with confidence. Ultimately, taking deliberate, strategic steps now—no matter your stage of life—positions you to enjoy a comfortable, financially stable retirement with fewer uncertainties and greater peace of mind.